The Architecture of Equilibrium: Mastering the Rebalancing Act

The Architecture of Equilibrium: Mastering the Rebalancing Act

In the early stages of building a financial fortress, most of the heavy lifting is done by the savings rate.

You shovel capital into the engine, and the sheer volume of fuel dictates the speed.

However, as a portfolio matures and enters the mid-to-late stages of compounding, a new and subtle challenge emerges.

The market, in its erratic brilliance, begins to pull your carefully crafted structure out of alignment.

This is the phenomenon of “Asset Drift,” and the discipline required to correct it is known as Rebalancing.

It is the only time in finance where you are systematically forced to sell your winners and buy your losers—a task that is mathematically simple but psychologically grueling.

The Geometry of Risk Drift

Imagine an investor who, after much soul-searching, decides on a “Moderate” allocation: 60% Equities (for growth) and 40% Fixed Income (for stability).

In a roaring bull market, stocks might return 20% while bonds remain flat.

By the end of the year, that 60/40 split has naturally drifted to 68/32.

On the surface, the investor is thrilled; the portfolio is larger.

But beneath the surface, the “Risk Profile” has fundamentally changed.

This individual is now carrying significantly more equity risk than their original plan allowed.

If a market crash occurs the following year, they will suffer a much deeper wound than they are prepared to bleed.

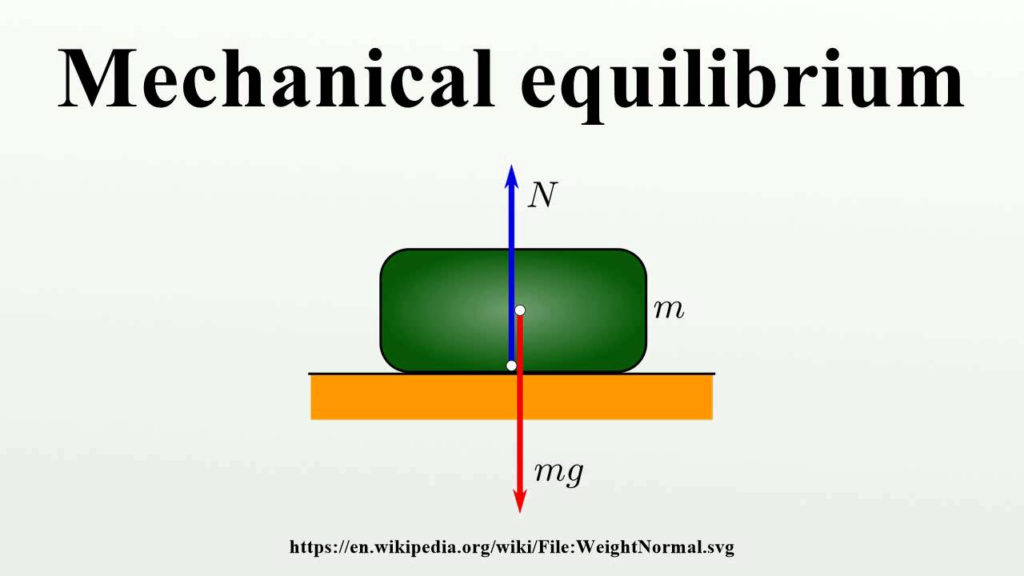

Rebalancing is the “gyroscope” that returns the ship to its intended course.

It ensures that your success doesn’t inadvertently turn you into a gambler.

The Three Rituals of Realignment

How and when should an architect of wealth intervene? There are three primary strategies for rebalancing, each with its own tactical merits:

-

The Calendar Method: You choose a specific date—perhaps the first of the year or your birthday—to reset the scales.

It is low-maintenance and removes the need for constant monitoring.

The Threshold Method (Tolerance Bands): You set a “boundary,” such as 5%.

If your 60% stock allocation hits 65% or drops to 55%, you trigger a trade.

This is more responsive to extreme market volatility but requires more frequent “health checks.”

The Inflow Method: This is the most elegant and tax-efficient strategy.

Instead of selling winners (which might trigger capital gains taxes), you use your new monthly contributions to buy only the underperforming asset class until the original balance is restored.

You are essentially “buying the dip” every month with fresh capital.

The Psychological Counter-Intuition

The true difficulty of rebalancing is not the math; it is the “Moment of Execution.” Rebalancing requires you to take money away from the “Star Performer”—the tech fund or the emerging market that is currently making you feel like a genius—and move it into the “Laggard”—the boring bond fund or the stagnant value stock that feels like a lead weight.

Our biological instincts scream against this.

We want to “let it ride.” We suffer from “Recency Bias,” believing that what went up yesterday will surely go up tomorrow.

But the history of the capital markets is a history of “Mean Reversion.” What is “hot” eventually cools, and what is “ignored” eventually finds its day in the sun.

Rebalancing is the mechanical tool that forces you to buy low and sell high, even when every fiber of your being wants to do the opposite.

The “Rebalancing Bonus”

While the primary goal of rebalancing is risk management, in certain volatile (but sideways) markets, it can actually provide a “return bonus.” By harvesting gains at local peaks and redeploying them into local troughs, you are effectively increasing the number of shares you own over time.

Think of it as a “Volatility Harvest.” You are turning the market’s nervous energy into a source of long-term profit.

Over a thirty-year horizon, the cumulative effect of these small, disciplined adjustments can result in a significantly higher ending balance with substantially lower overall volatility.

It is the closest thing to a “free lunch” in the investment world.

Tax Efficiency and the “Friction” of Change

For investors in taxable accounts, rebalancing must be handled with surgical precision.

Every sell order is a potential tax event.

This is why “Tax-Advantaged” accounts (like 401(k)s or IRAs) are the ideal laboratory for rebalancing; you can swap assets within the “wrapper” without the tax man taking a cut.

In a taxable account, the “Inflow Method” mentioned above is the primary weapon.

If that isn’t enough to correct the drift, one must weigh the cost of the tax bill against the risk of being over-exposed.

Often, a “partial rebalance”—moving the needle halfway back to center—is the most efficient compromise.

The Zen of the Plan

Ultimately, rebalancing is an act of humility.

It is an admission that we do not have a crystal ball.

We do not know which sector will dominate next year, so we maintain our “All-Weather” structure.

It transforms the investor from a “hunter” looking for a kill into a “steward” tending a garden.

By committing to a rebalancing ritual, you divorce your net worth from your ego.

You stop asking “What is the market doing?” and start asking “What does my blueprint require?” Wealth is built by those who can remain rational when the crowd is emotional.

Rebalancing is the physical manifestation of that rationality.

It is the quiet, repetitive work that ensures your financial house stands long after the storms of the present have passed.